Case Study

Crafting a 10b5-1 Plan

Matt and Rachel, 50 and 48 respectively, started working with Heritage Wealth Architects during a busy time in their lives. Both working professionals, Matt and Rachel, also have two kids who were busy with school and gearing up for college.

Busy managing their work and family lives, the couple came to Heritage Wealth Architects to help manage their investments and overall financial life. Upon an initial review of their investment accounts, the team discovered that Rachel was routinely granted non-qualified stock options, restricted stock units, and performance stock units as part of her total compensation package with her employer. Although Rachel had a general idea of what these were, she agreed that she could use help developing a strategy for capitalizing on these and understanding the tax implications.

NSO

Gives employees of a company the option to purchase the granted quantity of company stock at a designated strike price.

PSU

Company stock awarded to employees with a vesting schedule based on the attainment of certain performance goals by a pre-determined schedule.

RSU

These are units representing shares of company stock that are granted to employees as part of their compensation package.

We met with Rachel and Matt to go through Rachel’s plan site together and reviewed the options she had as well as the vesting schedule for her Restricted Stock Units. We discovered that she had a non-qualified stock grant expiring in the upcoming year. In addition, she owned several shares of stock that were at a loss position from where she had purchased it. Given that Matt and Rachel had limited flexibility with their cash flow, we devised a plan by which we sold some of her existing stock and used the proceeds to purchase the stock in the option. We also weighed this option in the broader context of their financial plan and found that their total income expectations for future years would be higher, making this year an ideal year to exercise the options.

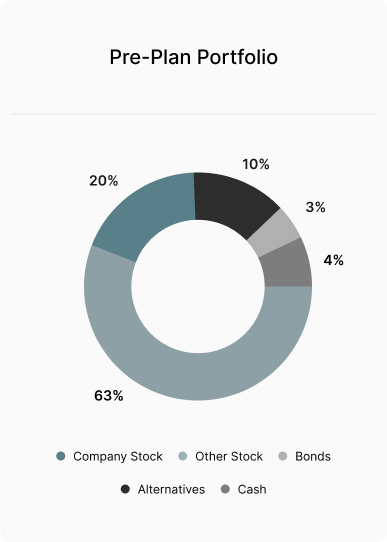

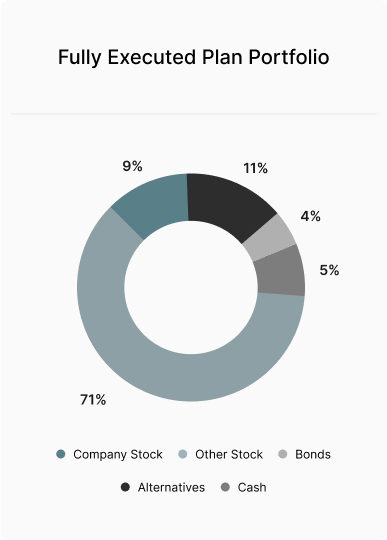

To do this, we worked with the third-party administrator to understand the plan rules and file the 10b5-1 plan as rules differ from company-to-company. The added benefit to filing the plan was that it signaled to the company confidence in the stock and Rachel’s investment in the company as she ended up with more stock than she started with pre-transactions. As part of the plan, we also opted to include a sale of the company stock that Rachel already owned at various price targets. These moves not only helped to strategically diversify out of the large concentration of company stock in Rachel and Scott’s portfolio, but also helped to ensure more security as the former options were now owned by Rachel outright. Should she choose to leave the company, the stock would not be forfeited.

With an understanding of their goals, future expenses, and cash flow, John and Samantha know what to do when their bonus arrives or when a considerable expense appears, removing uncertainty and complexity. Any money accumulated beyond this can be invested into their portfolio and help them further accomplish their retirement goal.

Ultimately, this move helped to reiterate to Rachel’s company that she was a strategic thinker who believed in the future of the company while diversifying her overall investment portfolio. In the context of Rachel and Matt’s broader financial plan, this also helped to position them better for retirement, saving them taxes and capitalizing on the options at the same time.